How to Accept Bitcoin Payments as a Freelancer or Small Business

Accepting Bitcoin. No Middleman. What does that look like?

If you freelance or run a small business, at some point you have probably thought about accepting Bitcoin. Maybe a client asked. Maybe you are just curious. Either way, the first question is usually not "why should I?" — it is "what does this actually look like?"

That is a better question anyway. The "why" stuff tends to turn into ideology pretty fast. The practical side is more interesting.

You do not need a payment processor

This is the part that surprises people who are used to things like Stripe or PayPal.

With cards and traditional rails, a payment processor is not optional. There is always somebody in the middle — taking a cut they expect you to absorb, applying chargeback rules, deciding when you actually get your money, and occasionally deciding you do not get it at all. With Bitcoin, you have a choice. There are Bitcoin payment processors and services you can use if you want one, but the underlying network does not require any of them. You can receive a payment without one.

That choice sounds like a small thing until you have had a payment processor freeze your account, or hold a deposit for "review," or charge you 2.9% plus thirty cents on a $50 invoice. For small operations, those fees and delays are not a hit you keep accepting. They add up fast enough to hurt.

The Bitcoin network itself has no payment processor role built into it. When a sender pays, the on-chain fee they include goes to miners — that is the cost of getting the transaction recorded, not a service fee. Once a payment confirms on-chain, it cannot be clawed back or reversed.

That does not mean accepting Bitcoin is free of overhead. You still need a way to generate invoices, track payments, and know when something has actually settled. The tools that handle those pieces vary — some sit lightly on top of the network, some are more involved. Some are free, some charge a fee, and the model often depends on what you need. We will get to that. The important point here is that the underlying payment does not depend on any one company being in the middle.

The volatility question

This is the elephant in the room and it is worth being honest about.

You quote a client $500. They pay in Bitcoin. By the time you convert it, or by the time you check the price a day later, it might be worth $480. Or $530. That kind of movement is normal for Bitcoin, and if you are running a business with actual expenses, unpredictable swings in what your receivables are worth is a real problem.

The way most freelancers and small businesses deal with this is USD-denominated invoicing. You set the price in dollars. The tool you use calculates the Bitcoin amount at the current exchange rate when the invoice is created. The client pays that Bitcoin amount. You received what you quoted, in Bitcoin, pegged to the dollar value at the time.

It does not eliminate volatility entirely — there is still a window between when the invoice is created and when the payment confirms — but it shrinks the exposure from "who knows" to a narrow, predictable window.

If you plan to hold Bitcoin long-term, volatility is part of the deal and you have already made peace with it. If you have not, USD-denominated invoicing keeps your pricing stable; that said, you will still want a plan for converting to dollars. Sweeping strategies, converting Bitcoin to dollars on a schedule that works for you, are worth looking into.

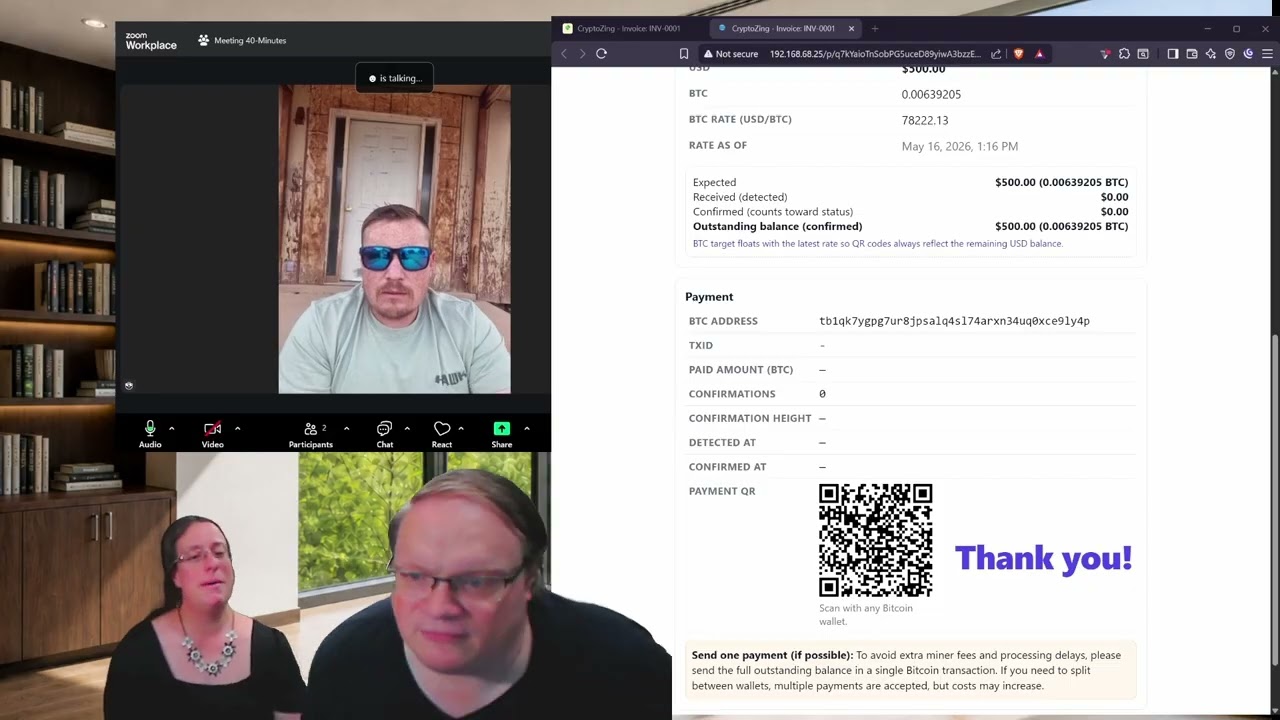

What a Bitcoin invoice actually looks like

If you are thinking of a bill in an envelope, that is the wrong picture. A Bitcoin invoice is a live payment request. Picture a checkout screen, not a piece of paper.

It is usually a QR code or a clickable link that encodes a Bitcoin address, an amount, and sometimes an expiration window. The client opens it in their wallet, confirms the amount, and sends.

From the client's side, it looks something like: scan, verify, send. From your side, it looks something like: create invoice, share the link, wait for the payment to show up, then wait for confirmation.

The mechanics are not complicated. The part that takes some thought is what happens between "the payment showed up" and "I can trust that it is settled." Bitcoin transactions go through a pending stage before they are confirmed on-chain. If you have read about how Bitcoin confirmation works, this is where that applies.

For most ordinary invoices, you are probably watching for one to three confirmations. Bigger amounts, you might want more. The point is that "I can see a payment" and "the payment is settled" are different things, and your workflow should account for that.

Who holds the money?

This is a question that rarely comes up with traditional invoicing because the answer is always "your payment processor, until they release it to you."

With Bitcoin, we have a choice.

Custodial tools mean someone else holds the Bitcoin for you. You get a dashboard, you can see your balance, and at some point you withdraw. This is convenient, but it also means you are trusting a third party with your money. If they get hacked, lock your account, or go under, your funds are at risk. You have probably heard stories.

Noncustodial tools send the Bitcoin directly to your own wallet. You hold the keys. Nobody else can touch it. The tradeoff is that you are responsible for your own wallet security — and that responsibility is real. Use a reputable wallet, back up your seed phrase, and keep your keys private. Do that and it is not nearly as scary as it sounds.

This is more significant than it seems at first glance, especially for a small business. The whole point of accepting Bitcoin is that it is supposed to be more direct and less dependent on intermediaries. Using a custodial service puts an intermediary right back in the middle.

Bookkeeping and taxes

Not the fun part, but it comes with the territory.

Receiving Bitcoin as payment has tax implications that vary by jurisdiction. Think of it like receiving payment in a foreign currency. USD-denominated invoicing helps because the dollar value is already baked in.

Talk to an accountant or look into crypto tax services. Keep records. Future you sends your thanks through time.

So is it complicated?

It used to be. The lack of good tooling meant it was mostly restricted to hard-core nerds. That has changed — modern tools handle enough of the mechanics that the interesting part is choosing your setup, not wrestling with it.

The actual flow is: set up a wallet, pick a tool that generates invoices, share payment links with clients, and watch for confirmations. The right tool makes most of that feel obvious.

Watch

How to Invoice Someone in Bitcoin

Watch

How to Invoice Someone in Bitcoin

The real question is not whether you can accept Bitcoin. It is whether your clients would use it. If even one or two would, it is worth exploring. And if you are the kind of person who likes the idea of getting paid without a middleman deciding when you get your money — well, that part is exactly as good as it sounds.